China’s latest five-year blueprint places power system reform, offshore wind, and hydrogen-based fuels at the core of industrial policy, reshaping investment flows, system economics, and global clean energy supply chains.

The newly released 15th Five-Year Plan (15th FYP, 2026–2030) formally embeds, for the first time, the goal of “building an energy superpower” into the national development strategy. This marks a pivotal shift in how the world’s largest energy consumer advances to balance decarbonization, energy security, and industrial competitiveness through 2030 and beyond.

The plan positions renewable energy not merely as a supplement, but as the key pillar of the future energy system. It arrives at a critical juncture, as China prepares for a structural transition toward a system in which non-fossil sources could exceed 80% of total energy consumption by 2060.

A structural upgrade of China’s energy strategy

The elevation of “energy superpower” status to a top-level policy objective signals a transition from incremental decarbonization to systemic transformation. The 15th FYP positions the next five years as decisive for building a New-Type Energy System (NTES), anchored by three priorities:

- Scaling renewable energy from incremental growth to a dominant supply

- Accelerating end-use electrification across industry, transport, and buildings

- Developing hydrogen and hydrogen-derived fuels as cross-sector decarbonization vectors

A critical commitment underpins these priorities: the majority of incremental electricity demand through 2030 will be met by new renewable generation, tightening the linkage between economic growth and clean power deployment.

Exponential scaling meets binding system constraints

The next phase of expansion is not simply about adding capacity; it is about managing complexity at scale. As renewable penetration rises, system integration, flexibility, and cost optimization become defining challenges.

In addition, offshore wind, particularly in deep-water environments, is emerging as a key lever to optimize resource quality, proximity to China’s economic centres, and overall system efficiency.

I. Renewable capacity expansion

China’s long-term modelling underscores the scale of ambition:

- Wind capacity: from 520 GW (2024) to ~3.3 TW by 2060

- Solar PV capacity: from 890 GW to 5.5–6.5 TW in the same period

By 2060, wind and solar could supply ~77% of electricity generation, with total renewables exceeding 90%.

Near-term (2030) milestones include:

- ~3 TW combined wind and solar capacity

- ~30% share of electricity generation from wind and solar

This trajectory places China well ahead of most global benchmarks, reinforcing its central role in supply chains for turbines, solar modules, and grid infrastructure.

II. Electrification of end-use sectors

Electrification is positioned as the primary mechanism for translating clean power into emissions reductions:

- The electrification rate reached 28.8% in 2024, already above major OECD economies

- Expected to reach ~35% by 2030, exceeding OECD averages by 8–10%

- By 2050, electricity could account for over 50% of final energy consumption

This implies rapid scaling of electric vehicles, industrial electrification, and digitally enabled demand-side management systems.

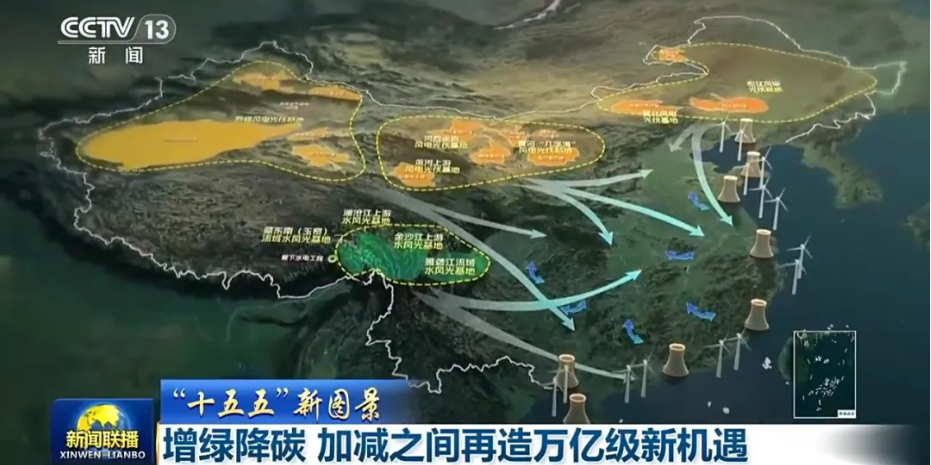

III. UHV transmission: enabling large-scale resource allocation

As renewable capacity expands geographically, grid infrastructure, particularly ultra-high-voltage (UHV) transmission, becomes a critical enabler of system integration.

On March 30, construction began on the Panxi UHV AC project, with a total investment of approximately CNY 23.2 billion and expected completion in 2028. As the first UHV AC project launched under the 15th FYP, it signals a new phase of accelerated grid expansion.

The project will serve as a key corridor for exporting clean energy from the Panxi region while helping rebalance Sichuan’s power flow structure and strengthening connectivity within the Chengdu–Chongqing economic cluster.

It also reflects a broader national push. In 2026, State Grid is advancing multiple UHV projects, including the Zhejiang AC ring network, Datong–Huailai–Tianjin South, Aba–Chengdu East, and the West Inner Mongolia–Beijing–Tianjin–Hebei corridor, alongside 750 kV projects such as Karamay.

By 2030, China aims to exceed 420 GW of west-to-east transmission capacity, reinforcing the grid’s role as the “arterial system” of resource allocation. Regional plans underscore the scale: Inner Mongolia alone targets 12 UHV lines (“six AC, six DC”) to support large desert-based renewable energy bases.

IV. System cost dynamics: the integration challenge

As renewable penetration increases, system costs become the central constraint:

- Beyond ~15% renewable share in the generation mix

- Every additional 5% adds ~CNY 0.1/kWh (1.4¢/kWh) to system costs

This relationship is non-linear, with costs accelerating at higher penetration levels. Key drivers include:

- Grid balancing and flexibility requirements

- Energy storage deployment

- Curtailment mitigation

- Long-distance transmission expansion

The implication is clear: while the 14th FYP focused on reducing generation costs, the 15th FYP shifts the focus to system-level optimization through market reform, infrastructure build-out, and technological innovation.

Hydrogen and derivatives: from niche to strategic pillar

Hydrogen and hydrogen-based fuels are positioned at the centre of energy security and deep decarbonization and, bridging renewable power generation with hard-to-abate end-use sectors.

Planned production capacity:

- Green ammonia: ~20 million tonnes per year, with import substitution potential of ~1.77% reduction in oil import dependence and ~62.67% reduction in natural gas import dependence

- Green methanol: ~26 million tonnes per year, with import substitution potential of ~2.33% reduction in oil import dependence and ~82.79% reduction in natural gas import dependence

Carbon abatement performance: Compared with fossil alternatives:

- Green methanol: ~81% CO₂ reduction

- Green ammonia: ~81% reduction

- Sustainable aviation fuel (SAF): ~86% reduction

These characteristics position hydrogen derivatives as viable solutions for hard-to-abate sectors, including heavy industry, maritime shipping, and aviation.

A multi-trillion CNY investment cycle

The 15th FYP is not merely a policy framework; it is also a concrete industrial demand signal, catalyzing investment across generation, infrastructure, and advanced materials.

Offshore wind: a flagship growth sector

Offshore wind, particularly deep-sea wind, is emerging as a commercially significant pillar of the transition. Deployment is accelerating into deeper waters, where wind resources are significantly stronger than nearshore zones, improving capacity factors and long-term project economics.

Key targets and opportunities include:

- 100 GW cumulative offshore wind capacity by 2030

- ~CNY 170 billion in wind turbine demand

- ~CNY 220 billion in offshore engineering and installation equipment

- ~5,000 km of high-end subsea cables

Beyond power generation, offshore wind is expected to integrate with offshore hydrogen production and coastal industrial clusters, further expanding its strategic importance.

Integrated clean energy systems

The plan emphasizes coordinated, system-level development across regions:

- “Three-North” wind and solar mega-bases

- Southwest hydro–wind–solar hybrid systems

- Coastal nuclear power bases, which are currently heavily concentrated in China’s key economic provinces: Guangdong, Zhejiang, Jiangsu, and Fujian

- Offshore wind clusters, with Jiangsu’s current coastal cluster alone accounting for roughly 40% of China’s offshore capacity, followed by Guangdong and Fujian

This reflects a shift from isolated asset deployment toward integrated optimization of generation, transmission, and consumption across the country.

Power market reform and pricing

China aims to establish a national unified electricity market during the 15th FYP period, supported by:

- Market-based pricing mechanisms across generation types

- Transparent and predictable regulatory frameworks

- Improved oil and gas network coordination

These reforms are critical to unlocking private capital, enabling efficient dispatch, and supporting high renewable penetration.

Reshaping global energy and industrial systems

China’s energy strategy marks a shift from energy importer to system orchestrator. The sheer scale of deployment across offshore wind, solar, and hydrogen is set to reinforce its leadership in clean technology manufacturing, influence global pricing benchmarks, and shape technology standards and innovation pathways.

Beyond supply, hydrogen is emerging as a central platform for new industrial ecosystems, linking power generation with chemicals, transport fuels, and heavy industry. As the transition matures, the focus is shifting from cost reduction to system optimization, with priority areas including grid flexibility, digital energy management, cross-regional transmission, and sector coupling.

Structural imbalances between resource-rich western regions and demand-heavy eastern centres further elevate the role of hydrogen, positioning it as both a storage medium and energy carrier. By 2030, with around half of electricity expected to come from non-fossil sources, the defining challenge will not be capacity build-out, but how effectively this system is integrated, monetized, and scaled across industrial applications – with offshore wind and hydrogen at its core.