In 2025, Sungrow Power Supply quietly became the world’s most valuable solar company, driven not by its legacy inverter business, but by a surging energy-storage segment built on data, software, and an asset-light manufacturing model.

This inflection point signals not merely a company-level shift but an industry-wide turning point in how value is created in solar energy. Globally, a broader trend is underway: the attempt to out-manufacture China is fading, giving rise to a paradigm where developers depend on integrated Chinese renewable energy solutions.

Sungrow’s Pivot: Software-Defined Storage Surpasses Legacy Inverters

In the first half of 2025, Sungrow’s operating income rose 40% to CNY 45.5 billion, with energy-storage systems (ESS) contributing 40.9% of revenue, surpassing inverters at 35.2% for the first time. The company also overtook LONGi, the long-time global champion of capital-intensive solar technology, to become the most valuable solar company by market capitalization.

This milestone reflects a strategic shift by Chinese companies. Rather than vertically integrating battery-cell manufacturing, which requires massive capital expenditure, Sungrow has adopted a low-capex sourcing strategy, purchasing lithium-ion cells from major Chinese suppliers such as CATL while allocating capital to software, system integration, smart energy management, thermal control, safety systems, and power electronics.

A high-quality battery cell does not automatically translate into a good product, and even a superior product does not necessarily deliver a compelling, scenario-level solution. Sungrow’s competitive edge lies precisely in its ability to bridge these gaps.

At a deeper level, Sungrow’s rise illustrates a core principle: where a company positions itself in the value chain ultimately determines its ceiling. In the first three quarters of 2025, Sungrow’s overseas shipments accounted for 83% of its storage business, indicating its system-level capabilities travel better globally than hardware alone.

In the increasingly competitive ESS market, Sungrow now sits alongside Tesla as one of the top shipment leaders. According to the latest industry rankings, Tesla remains the leading global ESS integrator with about 15% market share, followed closely by Sungrow with roughly 14%, CRRC Zhuzhou with around 8%, and then BYD, Huawei, and Envision.

Envision, another Chinese renewable-energy heavyweight, is pursuing a similar ESS-centric strategy while maintaining leadership in wind-turbine manufacturing. It has delivered more than 30 GWh of storage capacity and secured over 50 GWh in global orders. Envision is also expanding integrated offerings, including grid-forming systems and advanced energy-management software, alongside its wind portfolio.

China: The Hardware Foundations

The success of Sungrow and Envision is underpinned by China’s intense and resilient manufacturing base. Their software-driven strategies are fully integrated with China’s hardware dominance – leveraging scale, speed, and cost advantages that are difficult to replicate elsewhere.

I. Highly Automated Production at Scale

China’s manufacturing scale is extraordinary. Factories operate as tightly integrated ecosystems where materials, equipment, labour, automation, intelligent control, and logistics work together to achieve unparalleled economies of scale.

High-capacity plants bring new production lines online in weeks, rather than months or years in Europe, supported by dense equipment-supplier networks and deep engineering talent pools. This speed-to-scale reduces development cycles and accelerates learning curves.

At CATL’s gigafactories, dozens of high-throughput lines operate with minimal human intervention, from slurry mixing to module assembly. Combined with rapid iteration in sodium-ion and semi-solid technologies and advanced platforms such as the Kirin high-energy-density cell, this ecosystem drives dramatic cost down. These structural advantages have pushed battery-pack costs in China to roughly $60/kWh, about half those in Europe and the US, making pure manufacturing competitiveness elsewhere extremely challenging.

II. New Frontiers: Perovskites, SSB and Beyond

Building on its market dominance, China is rapidly extending its edge into next-generation frontiers. UtmoLight, which in 2022 built the world’s first GW-scale perovskite production line, has deployed several MW-scale perovskite PV projects in some of China’s harshest environments and has already exported its products to Japan. Other players, such as GCL, a global silicon producer, have shortened the transition from lab breakthroughs to pilot production in perovskites from years to mere months.

China is also rapidly advancing solid-state batteries (SSB), with multiple domestic players pushing pilot production. Major battery makers, including CATL, BYD, and Gotion High-Tech, are preparing pilot and small-series SSB lines, targeting energy densities above 400 Wh/kg and commercial demonstration by around 2027.

All of these reflect China’s supply-chain density: ready access to materials, talent, and advanced manufacturing equipment enables rapid industrial maturation.

III. Intelligent Manufacturing Solutions

China’s clean-energy dominance is reinforced by sophisticated automation providers supplying robotics, sensors, metrology tools, and turnkey production lines. Their ability to deploy customized systems on tight timelines lowers capex, boosts uptime, and accelerates iteration across the sector.

Notably, Wuxi LEAD Intelligent Equipment Co., Ltd. (LEAD), founded in 2002, has emerged as a prominent global leader in intelligent manufacturing equipment across PV, batteries, ESS, hydrogen, and automation fields, serving major clients in more than 25 countries.

In 2023, Wuxi LEAD delivered the industry’s first 20 GWh fully automated ESS container assembly line, advancing PACK assembly automation and enabling large-scale industrialization. Its integrated solution supports both CTP and MTP processes and incorporates AGV-based smart logistics, 3D and AI vision systems, AI algorithms, and advanced process simulation to deliver a fully automated, end-to-end assembly process from cells to containers, improving overall efficiency by 35% compared with traditional semi-automated lines.

In 2023, the company completed a lithium battery production line in Europe in just four months, custom-built for battery manufacturer InoBat. The line, comprising 35 state-of-the-art machines, adopts the latest high-speed stacking technology and covers the entire production process from cathode and anode slurry preparation to final formation and capacity grading.

Globally, Wuxi LEAD has established strong partnerships with Volkswagen, Mercedes-Benz, BMW, Audi, Tesla, SK, and Sony. In 2024, it delivered a customized solid-state, dry-electrode coating system to a leading Korean battery manufacturer, with an integrated solution that incorporates advanced buffer-component forming for cell structures, separator-free stacking, and continuous densification.

IV. China’s New-Energy Industry Ecosystem

China’s clean-tech cost advantage is structural, driven by gigafactory-scale production, cost-efficient equipment, dense supply chains, supportive policies, and rapid deployment. Its ecosystem functions as a unified, speed-optimized industrial organism.

The Yangtze River Delta region, including Shanghai, Jiangsu, and Zhejiang, is China’s epicentre of clean-energy manufacturing. It hosts leading battery, PV, hydrogen, and equipment enterprises; world-class R&D centers and infrastructure; and unmatched engineering talent, forming arguably the most efficient clean-tech supply chain on Earth.

Located at the center of the region, Wuxi stands out as a regional powerhouse, combining deep-tech manufacturing with advanced automation. Home to major equipment providers such as Wuxi LEAD and a dense ecosystem of component, material, and technology developers, the city is a strategic hub for domestic and international clean-energy players, driving innovation, rapid industrial scaling, and end-to-end solutions.

V. Profit Pools at the Next Frontier

At the next frontier, China aims to build globally competitive software platforms, shape international ESS, AI-grid, and hydrogen standards, and evolve industrial champions into ecosystem leaders.

- Current (2025): Cells, components, modules, and electrolyzers are commoditizing, while LDES, ESS systems, and software services are rising.

- Future (2026–2030): Profit pools will migrate toward AI-driven operations, transactive energy, renewable PPAs, storage-as-a-service, and integrated cross-border solutions.

Hardware remains essential, but value is moving decisively up the stack. Sungrow exemplifies this trend: global investors now prioritize system intelligence over raw production, creating a hybrid dynamic of “European software, Chinese hardware.”

Europe: The Software Opportunity

To meet 2030 climate goals, Europe requires massive deployment of green hydrogen, terawatt-scale solar and wind, and hundreds of GWh of energy storage. Yet European hardware ecosystems lack the scale and cost base to support this ambition. The pragmatic path forward is to leverage global supply chains while building leadership in standards, services, and software.

I. A Low-Capex Value-Capture Model

By outsourcing unit-level hardware to reduce capex and focusing on system-level intellectual property, European innovators can capture value in software, system architecture, project execution, and field-proven integration. This mirrors patterns observed across other technology sectors, where hardware commoditizes and margins migrate upstream into software and services.

Data is becoming a decisive differentiator. As storage, AI-grid, and renewable assets scale, advantage shifts toward predictive algorithms, digital twins, grid-aware control, and safety analytics. Ultimately, those who control system-level data are best positioned to capture the profit pools.

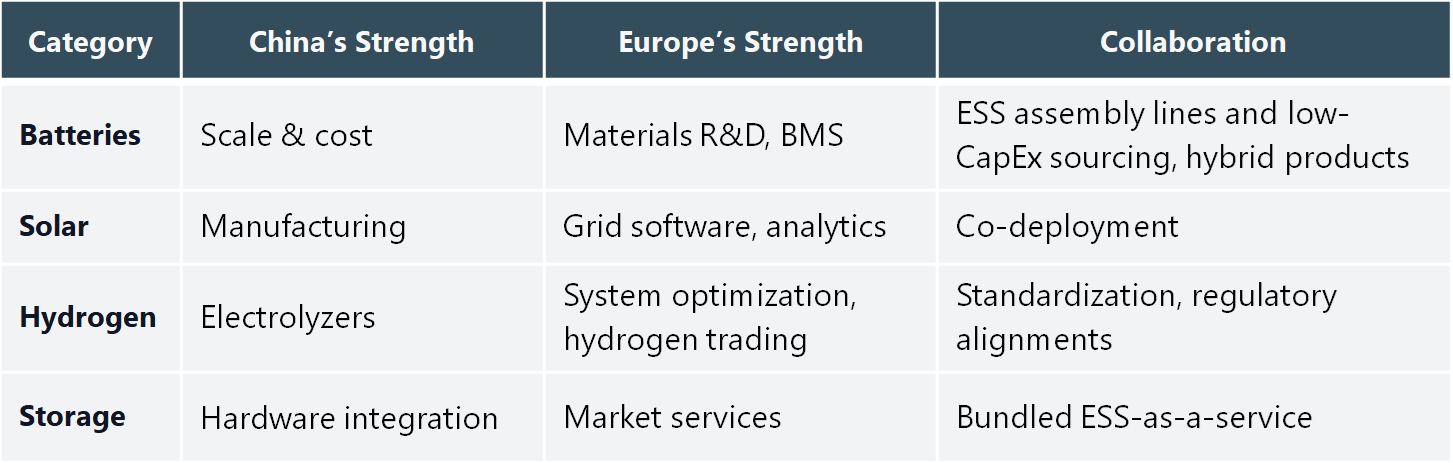

II. “Western Software, Chinese Hardware” as a Pathway

A hybrid model is emerging: Western companies lead in algorithms, grid integration, markets, and digital services, while China supplies cost-efficient, scalable hardware. This evolution parallels earlier shifts in semiconductors and consumer electronics.

European current strengths include:

- Control and energy-management software

- Predictive maintenance and virtual power plants (VPPs)

- Grid orchestration and flexibility services

- Carbon and energy market intelligence

- Battery-as-a-Service (BaaS) and asset-light business models

III. Europe–China Alignment: A New Industrial Paradigm

China’s manufacturing advantage, rooted in scale, speed, and dense supply chains, creates a platform for higher-value innovation. For both European and Chinese players, the strategic response is to build on this foundation, turning manufacturing strength into software, systems, and service-led value.

In this context, Wuxi LEAD serves as an accessible “manufacturing equipment platform,” enabling both European and Chinese companies to move seamlessly from prototype validation to pilot lines and GW-scale production. Through modular, flexible, and rapidly deployable manufacturing solutions, the company lowers barriers to commercialization, shortens time-to-market, and allows innovators to focus on technology differentiation rather than building manufacturing capabilities from scratch.

The future of clean tech will be shaped not by isolated technologies, but by system-level efficiency and cross-border collaboration. Those who embrace the hybrid model, European software paired with Chinese hardware, are likely best positioned to define the next phase of the global energy transition.