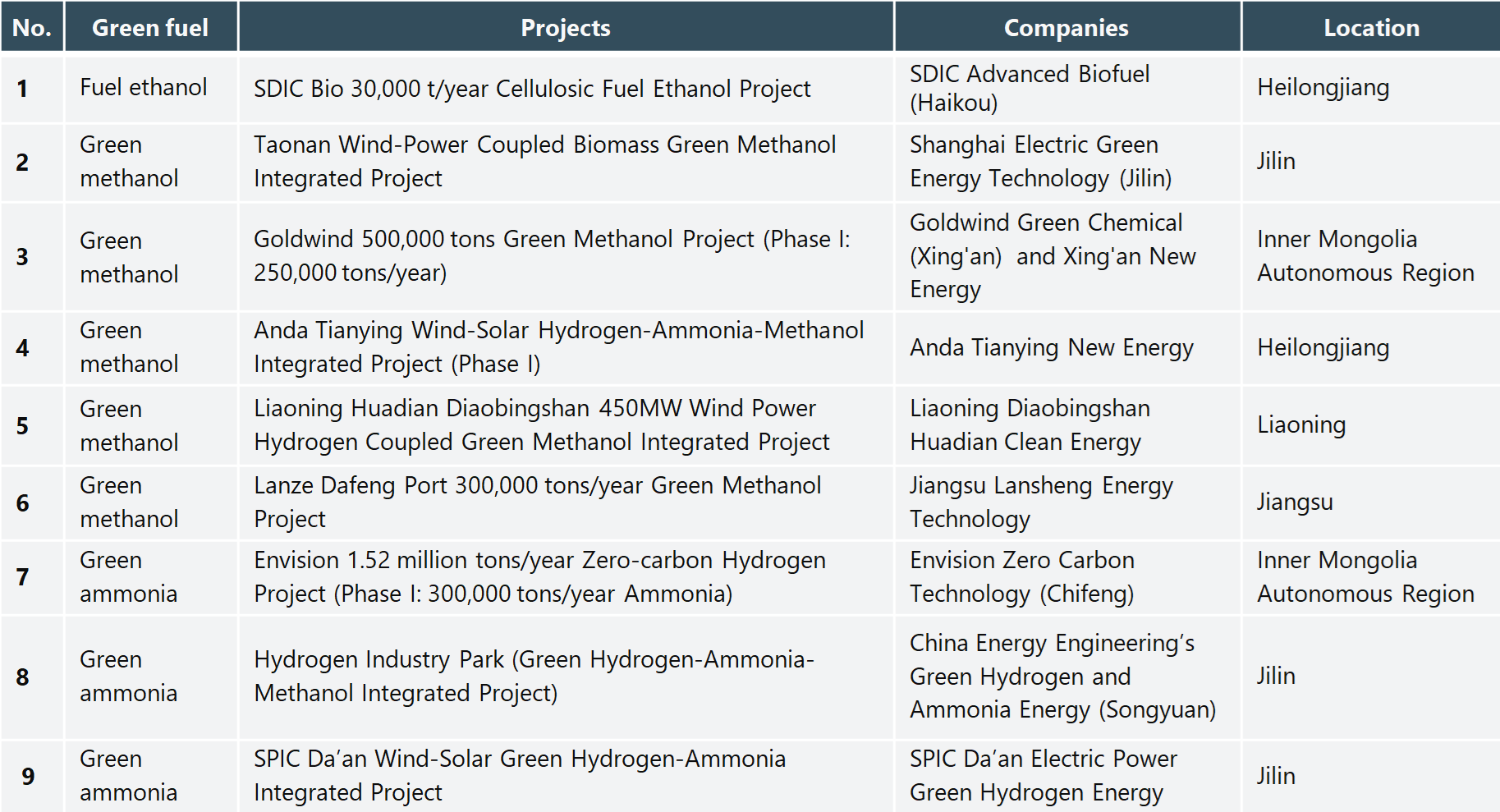

On September 5, China’s National Energy Administration (NEA) released the first batch of pilot projects under its Green Liquid Fuel Technology R&D and Industrialization program. As shown in the table below, the batch includes nine projects: one on cellulosic fuel ethanol, five on green methanol, and three on green ammonia.

The pilots aim to accelerate technology breakthroughs and advance commercial readiness in green liquid fuels, focusing on renewable integration, efficiency, and large-scale industrial deployment. Selected projects are expected to be completed and operational by the end of 2026, with full-scale production achieved by June 2027.

Regions and Scales

The projects are concentrated in Northeast China, which hosts six projects (three in Jilin, two in Heilongjiang, and one in Liaoning) and two in Inner Mongolia, while the only southern project is in Jiangsu Province. This distribution aligns with resource availability: Northeast China offers abundant biomass, wind, and solar resources, as well as established industrial bases, while the Jiangsu project at Lanze Dafen Port leverages coastal logistics, market access, and regional innovation resources.

Project scales vary. Green methanol pilots range from 50,000 tons/year in Taonan to 300,000 tons/year at Lanze Dafen Port. Smaller projects focus on local resource conversion; larger ones target broader market supply and cluster development. Green ammonia projects are more uniform (180,000–300,000 tons/year), reflecting stable downstream demand and an integrated supply chain and cost efficiencies.

Implementation Entities

The projects involve strong public–private collaboration, including central state-owned enterprises (SOEs) such as State Development & Investment Corporation (SDIC), China Energy Engineering Corporation, and State Power Investment Corporation (SPIC); local SOEs (e.g., Shanghai Electric); and wind companies (e.g., Goldwind, Envision Energy). Traditional energy players provide industrial infrastructure, while renewable innovators contribute technical capabilities.

Technology Pathways

Green methanol technologies include biomass gasification (e.g., oxygen-blown pressurized fluidized bed and dry powder entrained flow gasification) and tail-gas hydrogenation (from biomass boilers or ethanol plant off-gas) to valorize industrial emissions and create circular production chains. Green ammonia focuses on flexible synthesis routes.

For example, the Liaoning project, a 450 MW wind-to-hydrogen and green methanol pilot, converts wind power into green hydrogen via ALK (3,000 Nm³/h per unit) and PEM electrolysis. Hydrogen reacts with biomass-derived CO₂ from a nearby ethanol plant to produce methanol, serving as a platform for large-scale R&D and closed-loop green hydrogen systems.

Policy Incentive Framework

To support the pilots, the NEA has designed a package of measures to derisk investment and encourage early adoption:

- Preferential medium- and long-term loans

- Eligibility under China’s “first set” major technical equipment policy

- Inclusion in the CCER carbon crediting mechanism for faster ecological value monetization

- Targeted R&D funding coordinated by the NEA and relevant ministries

Standards to Anchor Commercial Scaling

To complement the pilots, the NEA is developing technical standards for green methanol and ammonia. On July 27, 2025, it launched a public consultation on 2025 standardization projects, including ten hydrogen-related standards such as Guidelines for Planning and Design of Wind–Solar–Biomass-to-Green Hydrogen–Ammonia–Methanol Systems, scheduled for completion by 2027

The guidelines, drafted by a consortium including China Electric Power Planning & Engineering Institute, SPIC Energy Innovation (Jiangsu), two State Grid Research Institutes (Gansu & Fujian), China Power Engineering Consulting Group, Tsinghua University, Dingzhou RISUN Hydrogen, and China Tianying, will define key parameters for integrated renewable-to-fuel systems: resource assessment, site selection, capacity optimization, operational control, construction planning, performance evaluation, investment modelling, and environmental and socio-economic impact. The goal is to harmonize engineering approaches, reduce development risk, and facilitate bankable proposals domestically and abroad.

Market Outlook and Significance

The twin-track approach—pilots paired with standards—positions China to rapidly scale green methanol and ammonia. By linking policy support to technical compliance, the NEA is fostering a market-ready ecosystem that lowers capital costs for early adopters, boosts investor confidence through standardized risk assessment, enhances export potential to Belt and Road markets, and enables participation in carbon markets via CCER credits.

With industrial-scale pilots already underway and foundational standards scheduled for completion in 2027, the NEA’s programs represent a strategic inflection point in China’s decarbonization pathway for hard-to-abate sectors such as maritime transport, chemicals, and heavy industry.