On August 1, the National Energy Administration (NEA) released the China New-Type Energy Storage Development Report (2025). The report presents China’s rapid progress in scaling new-type energy storage (NTES). Key points for 2024 include:

- Capacity: By end-2024, China reached 73.76 GW/168 GWh of NTES, accounting for over 40% of global capacity.

- From pilots to grid assets: Average utilization rose to 911 hours, with NTES now delivering 200–250 annual cycles, multiple revenue streams, and proven grid-scale dispatch.

- Policy framework: The 2024 Energy Law legally defines NTES as core power infrastructure, while provinces pioneered market models that turned NTES into revenue-generating assets.

- Multiple tech pathways: While lithium-ion accounts for 96.4% of capacity, breakthroughs in sodium-ion, flow batteries, and compressed air storage are scaling.

- Cost and durability: Lithium system capex dropped below $200/kWh, with cycle life now above 15,000, setting new global benchmarks; VRFB system costs dropped ~20% YoY (vs. 2023).

China targets 100 GW by 2025 (already at 95 GW by H1 2025) and 300 GW by 2030, solidifying its position as a global leader in energy storage.

Rapid NTES Growth

China ended 2024 with 73.76 GW/168 GWh of NTES in operation, adding 42.37 GW in a single year and accounting for more than 40% of global installations.

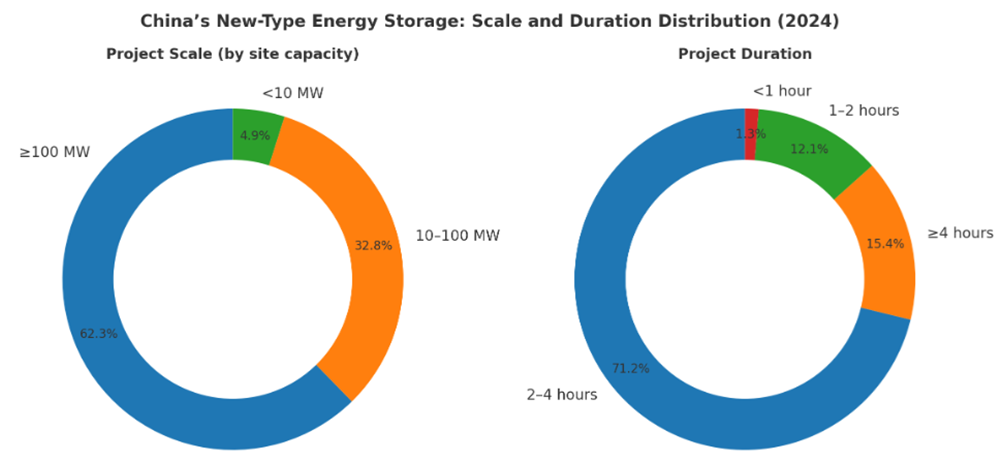

- Project scale: Large-scale and multi-hour projects dominate, with 62% exceeding 100 MW and 86% more than two hours duration.

- Utilization: Average operating hours reached 911 hours, up 300 hours from 2023.

NTES: Policy Framework

Released in 2024, China’s Energy Law defines NTES as a core component of power systems, marking a shift from policy guidance to legal codification. This strengthens investment certainty and aligns with China’s dual-carbon goals. Implementation has accelerated across provinces, with policies tailored to local market structures and resources. At the provincial level:

- Shandong: Led on capacity compensation and long-duration incentives.

- Guangdong: Introduced the “1+N+N” framework (i.e., one provincial policy guiding sectoral measures (1st N), further refined by city-level actions (2nd N).

- Jiangsu: Pioneered hybrid revenue models combining spreads, peak subsidies, and ancillary services.

- Zhejiang: Deployed NTES for seasonal reliability.

- Xinjiang: Integrated storage directly into desert wind-solar bases.

In 2024, State Grid and China Southern Power Grid launched the “Central Enterprise NTES Innovation Consortium” to drive R&D, standardization, and deployment. Backed by provincial support, the initiative moved NTES from pilots to commercially viable, revenue-generating assets, strengthening market confidence.

The chart below shows NTES utilization hours in eight provinces, 2024 vs. 2023.

Technical Outlook

China’s policy foundation has set the stage for technological diversification. While lithium-ion remains dominant, the emergence of sodium-ion, flow batteries, and compressed-air storage reflects a dual-track strategy: scaling proven technologies while fostering breakthroughs that could redefine cost and duration benchmarks.

Lithium Leads, Alternatives Rise

- Lithium-ion: Accounts for 96.4% of total installed capacity.

- Sodium-ion: World’s first 100 MW/200 MWh project (Qianjiang) achieved 80% efficiency and stable operation at –40 °C.

- Flow batteries: National capacity reached 560 MW (over CNY 4 billion invested); Jilin launched the first cold-climate 100 MW/400 MWh VRFB station. 70 kW-class high-power single stack developed; non-fluorinated ion-exchange membrane in pilot-scale production.

- Compressed air (CAES): Installed capacity surpassed 1 GW (over CNY 10 billion invested), with multiple 300 MW-class projects underway.

- Emerging options: CO₂, liquid air, and gravity storage completed first demonstrations with state R&D support.

- Next-gen technologies: Solid-state, hybrid thermal, and hydrogen-based systems remain at pilot scale but are progressing.

This multi-path approach mirrors China’s PV and EV success: mass deployment of proven solutions while encouraging cutting-edge avenues for future breakthroughs, with policy continuing to guide technology scale-up.

In August, the NEA released the Fifth Batch of First-of-their-Kind Key Energy Equipment, listing 82 items, including ten related to energy storage: lithium-ion, vanadium redox, zinc–bromine, semi-solid lithium-ion, polyanionic sodium-ion, compressed air, 35 kV networked systems for flexible grid integration, and dynamically reconfigurable battery systems (DRBS).

Alongside storage, wind–solar–hydrogen projects have scaled up rapidly: electrolysis capacity has surged from just 5 MW in 2015 to 4 GW in 2025. Within this shift, 35 kV systems have become the mainstream choice, reaching 67% market penetration. For a 1 GW project, adopting 35 kV instead of 10 kV typically improves system efficiency by 2–3% and lowers total system cost by 15–20%.

Lithium: Scale, Durability & Reliability

Lithium-ion batteries in 2024 achieved significant performance gains:

- Cell size: >500 Ah; 6 MWh/container systems are now standard

- Energy density: >400 Wh/L, reducing footprint

- Cycle life: >15,000 cycles, with lifetimes exceeding 15 years

- Thermal management: Immersion cooling limited temperature rise to <5 °C

- Grid-forming: 100 MW/200 MWh plants demonstrated black-start capability and fast fault recovery.

These advances supported higher utilization: average annual utilization reached 911 hours, up 300 hours YoY, with independent/shared projects exceeding ~1,000 hours and renewable-attached projects doubling to 766 hours. Commercially, storage assets now cycle 200–250 times per year (up from less than 150 in 2023), enabling multiple revenue streams and stronger bankability.

Market Scale and Economics

China accounted for more than 40% of global NTES capacity in 2024, exceeding the combined total of Europe and the U.S.

- Regional hubs: North China (22.2 GW) and Northwest (18.7 GW) together represent 55.5% of the national total.

- Provincial leaders: Inner Mongolia (10.23 GW), Xinjiang (8.57 GW), Shandong (7.17 GW), Jiangsu (5.62 GW), Ningxia (4.43 GW). Eleven provinces each added >1 GW in 2024.

- Capital flows: Flow batteries and CAES attracted over CNY 100 billion; sodium-ion moved from pilot projects to pre-commerializatoin.

- System costs: Lithium capex fell below $200/kWh, 20–30% lower than EU and U.S. peers.

- Revenue models: Largely market-driven. In July 2024, Jiangsu dispatched 4.5 GW of NTES, equivalent to a 900 MWh “super battery”, demonstrating commercial viability at grid scale.

China: The Global Testbed for NTES

China’s NTES boom has established it as a global reference for both technology and market design.

- Cost leadership: <$200/kWh and 15,000 cycles set global benchmarks

- Industrial policy edge: National laws, provincial innovation, and financing accelerate NTES deployment

- Diversification: Sodium-ion, CAES, and flow batteries reduce dependence on lithium.

- Supply chain leverage: China is positioned to replicate its success in solar wafers and EV batteries within energy storage.

2024 marked NTES’s transition from pilot projects to backbone infrastructure. With renewables surpassing coal, China’s grid stability increasingly relies on NTES, and its techno-business innovations are expected to shape the global storage landscape.