China added a record 268 GW of renewable energy capacity in the first half of 2025, according to data released by the National Energy Administration (NEA) on July 31. Renewable energy now accounts for 59.2% of total installed power capacity and nearly 40% of electricity generation, signalling the country’s accelerating clean energy transition.

China’s Renewable Capacity and Generation

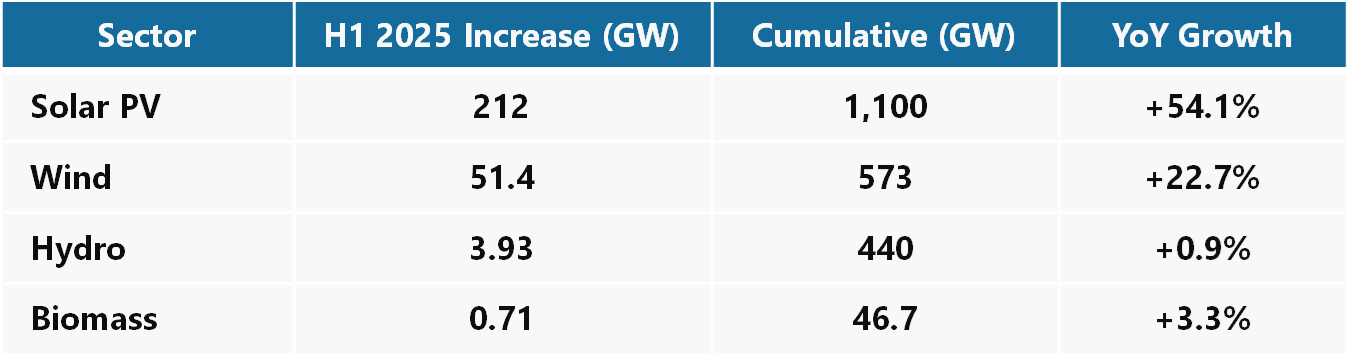

H1 2025 additions:

- Solar: 212 GW (100 GW grid-scale, 113 GW distributed)

- Wind: 51.4 GW (48.9 GW onshore, 2.49 GW offshore)

- Hydropower: 3.93 GW (of which 2.83 GW is pumped storage)

- Biomass: 0.71 GW

As of June 2025, China’s cumulative renewable capacity reached 2.16 TW.

H1 2025 renewable generation: 17,993 TWh (+15.6% YoY)

- Wind + solar: 11,478 TWh (+27.4% YoY), accounting for 23.7% of total electricity generation

- Utilization rates: Wind 93.2%, Solar 94%

- Hydropower: 5,398 TWh; average utilization: 1,377 hours

- Biomass: 1,117 TWh (+8.4% YoY)

Notably, renewable electricity generation exceeded the combined consumption of China’s tertiary (9,164 TWh) and residential (7,093 TWh) sectors—indicating that clean energy is no longer just meeting marginal or peak demand. Instead, it is now supporting base-load consumption at scale.

Deployment Patterns and Grid Integration

China’s strategy focuses on both scale and diversification:

- Solar additions were nearly evenly split between utility-scale and distributed systems, advancing electrification across rural, urban, and industrial areas.

- Wind growth remained onshore-dominant, though cumulative offshore wind capacity also rose, reaching 44.2 GW.

- Hydropower investment prioritized flexibility, with 70% of new capacity from pumped storage, enhancing the grid’s ability to integrate intermittent solar and wind generation.

These efforts are reinforced by grid parity policies, green finance mechanisms, and China’s vertically integrated clean energy supply chain.

Commercial Relevance and Export Impact

China’s massive domestic deployment is driving global impact:

- Levelized Cost of Electricity (LCOE):

- ~$25/MWh for utility-scale solar

- ~$30–35/MWh for onshore wind

- Grid parity achieved in nearly all Chinese provinces

- Solar exports: +35% YoY in H1 2025

China now accounts for over 80% of global solar module exports and around 60% of wind turbine exports. Scale-driven cost advantages continue to cement its role in global clean energy supply chains.

Strategic Implications

- Fossil Displacement: Wind and solar additions exceeded electricity demand growth, reducing the share of coal-fired generation.

- Storage & Flexibility Needs: While pumped hydro is growing, scaling up battery storage, LDES, hydrogen-based flexibility, and demand-side management will be essential.

- Global Technology Outreach: Lower domestic production costs are enabling clean energy transition in the global market, reshaping worldwide energy and trade dynamics.

Outlook

If current trends continue, China is on track to exceed 3 TW of renewable capacity well before 2030, bringing its dual carbon goals (peaking by 2030 and neutrality by 2060) within closer reach. Realizing this potential will require continued grid reform, market-based pricing, and stronger interprovincial transmission infrastructure.

For investors, technology providers, and policymakers, China’s H1 2025 performance sends a clear message: the global energy transition is accelerating, and China is once again leading the way.