In November 2025, China’s monthly sales of electric heavy-duty trucks reached 28,000 units, pushing market penetration to 36.45%. This marked the first time new-energy heavy trucks accounted for more than one-third of total heavy truck sales.

The milestone signals a structural shift in freight transport economics, driven by policy support, standardization, fast charging and battery swapping, and the expansion of electric trucking from ports and mines into open-road trunk routes of up to 800 kilometres.

For manufacturers, logistics operators, and energy companies, electric heavy trucks have moved from a subsidized niche to a competitive industrial system defined by scale, standards, and increasingly self-sustaining demand.

Truck Electrification From Closed Sites to Long-Haul Routes

Behind the aggregate data lies a story of how electrification is spreading across use cases. Closed and semi-closed environments – ports, steel plants, and mining sites –now report electrification rates above 60%. Short-haul open scenarios, such as construction waste and cement transport, have reached penetration rates of around 35%, often underpinned by local mandates. Most notably, pilot operations on long-haul trunk routes of 600–800 kilometres have progressed from demonstration to early commercialization.

Market leadership is also consolidating. In November, XCMG sold 3,963 electric heavy trucks, FAW Jiefang 3,715, and Sany 3,724, while Sinotruk posted the fastest growth rate at nearly 279%. Regionally, Shanghai led with nearly 30,000 units sold year to date, followed by Shanxi (12,000) and Hebei (11,000), with all 31 provinces reporting sales above 100 units.

Policy and Standards: From Incentives to Infrastructure Rules

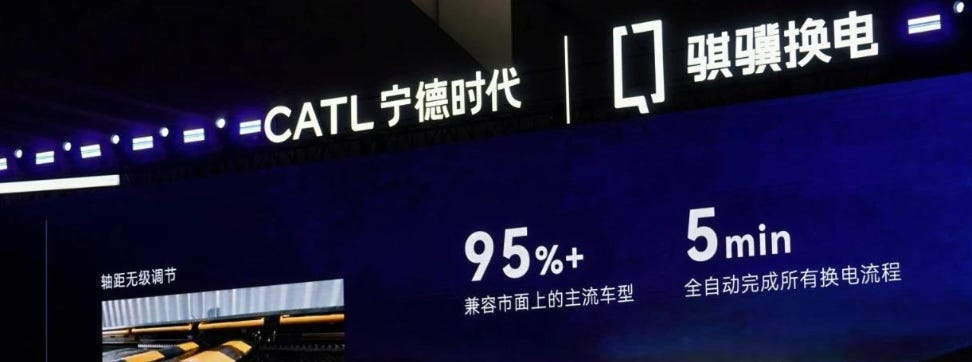

A key enabler of the November surge was standardization, particularly in battery swapping. On November 1, 2025, China implemented the national standard GB/T 40032.2-2025: Electric Vehicle Battery Swapping Safety Requirements, Part 2: Commercial Vehicles. The regulation codifies safety thresholds, battery design, and operational processes for heavy-duty battery swapping, including a requirement that a single swap be completed in six minutes or less.

The commercial significance lies in interoperability. The standard accelerates cross-brand battery compatibility, already demonstrated by battery-swapping heavy trucks from XCMG and Sany operating on the same routes in Linfen, Shanxi. For fleet operators, this reduces asset lock-in; for infrastructure investors, it improves swap-station utilization; and for manufacturers, it shifts competition toward vehicle efficiency and software rather than proprietary battery formats.

Safety and regulatory treatment have also tilted the field. Under China’s digital safety supervision framework, electric heavy trucks operating in closed environments have been exempted from certain high-risk classifications. In coal mines in Shanxi, this has lifted utilization rates to 95%, materially improving fleet economics relative to diesel.

At the local level, policy support has evolved beyond purchase subsidies toward operational advantages. Preferential road access, guaranteed dispatch volumes, and discounted electricity tariffs, often as low as CNY 0.30/kWh versus industrial rates of CNY 0.55/kWh, have become decisive levers, particularly for long-haul pilots.

Large-Capacity Batteries and Extended Range

The technical backbone of the current surge is the rapid scaling of battery capacity. Flagship models now routinely exceed 500 kWh. XCMG’s 801 kWh pure-electric tractor offers a real-world range of around 495 kilometres, while DeepWay’s 600 kWh platform achieves up to 670 kilometres under optimized conditions.

These specifications are reshaping the feasible operating envelope. On routes such as Shanxi–Shandong, roughly 800 kilometres end to end, electric trucks can complete a single trip with two intermediate energy replenishments via fast charging or battery swapping, without compromising payload or schedule reliability.

Energy recovery systems further extend the effective range. In mountainous corridors, regenerative braking can recover approximately 5 kWh per 10 kilometres of downhill travel, boosting overall range by around 15% in suitable terrain.

Charging and Swapping: Speed as a Competitive Variable

Energy replenishment speed has become a central performance metric. On the charging side, Huawei’s 1.44 MW liquid-cooled ultra-fast charging solution enables trucks to gain roughly 200 kilometres of range in 15 minutes. While still infrastructure-intensive, this significantly narrows the operational gap with diesel refuelling for certain duty cycles.

Battery swapping remains dominant in high-utilization scenarios. In mining operations, swap times of three minutes support up to 25 trips per day, delivering fleet efficiency estimated at 30% above comparable diesel trucks. The new national standard is expected to accelerate deployment along trunk corridors, where time reliability is paramount.

Total Cost of Ownership Turns Decisive

The most powerful driver of adoption in China is no longer policy, but economics. Across multiple scenarios, electric heavy trucks now demonstrate a clear total cost of ownership (TCO) advantage over diesel.

In ports such as Shenzhen’s Mawan terminal, where electric container trucks account for 85% of the fleet, operators report energy cost savings of approximately CNY 1,800 per trip compared with diesel. On an annualized basis, long-haul pilots show fuel savings equivalent to 10 million litres of diesel for fleets of around 200 vehicles.

Even with higher upfront vehicle costs, lower energy prices, reduced maintenance requirements, and higher utilization rates collectively generate lifetime savings of up to CNY 1.58 million per vehicle over five years. For drivers, these economics translate into higher net income, often CNY 8,000 more per month, driven by lower fuel deductions and more stable dispatch.

These dynamics explain why, even as subsidies begin to taper, market penetration is expected to continue rising toward 40% in 2026.

The Linfen, Shandong Case: From Closed Sites to Trunk Routes

The most strategically significant development in 2025 has been the commercial validation of long-haul electric trucking. A flagship example is the Linfen–Shandong port corridor, where a fleet of 200 electric heavy trucks operates on an 800-kilometre route under a “heavy outbound, heavy return” model.

Each truck completes the journey with two battery swaps, each taking approximately five minutes. Supported by government-backed charging and swapping stations and preferential electricity pricing, the fleet has reduced energy costs by 25% compared with diesel while maintaining schedule reliability.

Operationally, the model relies on more than hardware. AI-driven dispatch algorithms match vehicles and cargo flows to eliminate empty runs, reducing the industry’s typical empty-mileage rate of around 60% to effectively zero. The result is a dual-profit corridor: coal transported eastbound and port-related cargo moved westbound.

For policymakers, the case demonstrates that electric heavy trucks can support strategic freight flows, such as west-to-east coal transport, without sacrificing efficiency or resilience.

Market Structure and Business Models

The electric heavy truck value chain is evolving rapidly. OEMs are increasingly partnering with battery suppliers, energy utilities, and infrastructure developers to offer bundled solutions rather than standalone vehicles.

Charging-focused models account for 67.46% of cumulative 2025 sales (125,000 units), while battery-swapping models represent 30.52% (56,700 units). This split reflects a bifurcated market: charging dominates short-haul and regional logistics, while swapping gains traction in high-throughput and long-haul corridors.

New entrants such as DeepWay and Geely’s Farizon are pursuing ecosystem strategies, co-developing “eight horizontal, ten vertical” national battery-swapping networks with energy partners. Traditional manufacturers are hedging with hybrid platforms. Foton and FAW Jiefang, for example, are scaling hybrid heavy trucks such as the Auman Galaxy HEV, which claims fuel savings of 26% in mountainous terrain.

Hydrogen fuel cell trucks remain marginal, largely confined to demonstration projects, such as the deployment of 500 hydrogen heavy-duty trucks in Xinjiang, but continue to receive policy support as a long-term decarbonization option.

According to the China Hydrogen Fuel Cell Vehicle Industrialization Development Report (2025) released by CAAM this December, high costs remain the main barrier to large-scale FCV deployment. For a typical 49-ton hydrogen truck, the fuel cell system and hydrogen storage account for about 53% and 14% of total vehicle cost, respectively. CAAM projects that by 2027, the fuel cell system’s share will fall to no more than 40%, enhancing the commercial viability of hydrogen heavy-duty trucks in the coming years.

Competition and Capital

For manufacturers, the transition compresses development cycles and raises capital intensity. Battery costs, software integration, and energy partnerships now matter as much as driveline engineering. Scale is becoming decisive, favouring players able to amortize R&D across thousands of units and secure favourable energy contracts.

For logistics companies, electric heavy trucks shift competitive advantage toward operators with route density, predictable demand, and access to infrastructure. Early movers are locking in lower operating costs and preferential road access, potentially reshaping market share in bulk commodities and container transport.

At a system level, heavy-duty electrification carries material carbon implications. Heavy trucks account for a disproportionate share of road freight emissions. A 36% penetration rate implies millions of tonnes of annual CO2 abatement, reinforcing China’s broader industrial decarbonization strategy.

2026: From Policy-Driven to Market-Driven Growth

November 2025 will likely be remembered as the moment China’s electric heavy truck market crossed from policy experiment to market reality. With penetration exceeding 36%, the sector has entered a phase in which economics, rather than subsidies, are the primary driver of adoption.

The transition will test industry resilience. From 2026, purchase tax exemptions will be halved, and some local vehicle replacement subsidies will expire. Industry forecasts point to a short-term sales pullback of 10–15% in the first quarter, followed by stabilization as TCO advantages reassert themselves.

At the same time, technological competition will intensify. Energy density and infrastructure coverage are emerging as the key battlegrounds. The first manufacturer to industrialize solid-state batteries at around 400 Wh/kg would reset the performance frontier, enabling longer ranges with lower weight penalties. In parallel, the race to build a truly national, interoperable battery-swapping network will shape leadership in long-haul electrification.

For logistics companies, the window to secure both remaining incentives and structural cost advantages is narrowing. Early movers are locking in lower operating costs and operational privileges that may prove difficult to replicate. For drivers, electric heavy trucks offer tangible benefits: lower fatigue, quieter cabins, and higher take-home pay driven by reduced fuel costs and more stable dispatch.

For the industry as a whole, the rules of competition are being rewritten around energy efficiency, digital coordination, and ecosystem scale. The question is no longer whether electric heavy trucks will dominate China’s freight future, but which players will define the standards, networks, and technologies that shape the next decade.